The Growth Series 2026 | Week 27: The Convenience Channel – Micro-Format Growth and Out-of-Home Calories

Martin Bailie CEO & founder MWB advisory Ltd

"Convenience stopped being about proximity a long time ago. The channel that wins the next five years is the one that admits it isn't a small supermarket anymore—it's a quick-service restaurant that happens to sell fuel." Martin Bailie

We have systematically engineered operational velocity, mastered computer vision on the shop floor, and transformed physical space into premium media inventory. Now, we confront the structural transformation of physical proximity:

The Convenience Channel.

When I audit retail networks globally, the single most recurring strategic error is a basic identity crisis. Convenience stopped being about mere geographical proximity a long time ago. The operators who win the next five years will be those who accept an uncomfortable truth: you are no longer running a small supermarket—you are managing a quick-service restaurant (QSR) that happens to sell fuel.

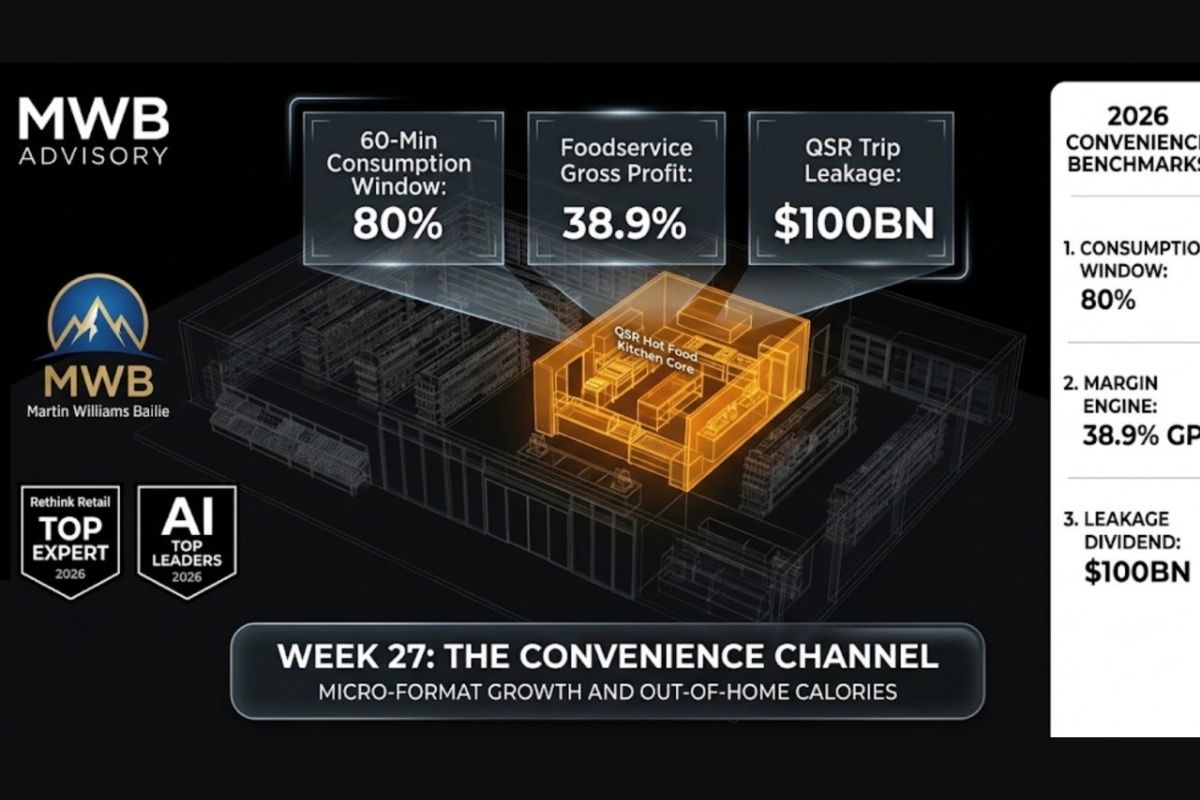

The “Agentic Leap” this week demands the immediate operational shift from a static footfall channel to an intelligent, demand-sensed consumption engine. IGD (Institute of Grocery Distribution) newly published Global Convenience Trends 2026 research draws the sharpest line yet between two entirely divergent futures for this format. The traditional “small supermarket,” rooted in top-up grocery missions, is losing relevance. Conversely, “pure convenience” is actively abandoning take-home groceries in favour of food and drink engineered to be consumed within the hour. Circle K internal operational metrics make the point starkly: roughly 80 percent of what it sells in-store is consumed within sixty minutes of the transaction. That is not a grocery retailer with a snacking aisle; that is a high-volume food business with a fuel pump attached.

The Bailie Diagnosis

“My diagnosis of the convenience sector is unyielding: too many boards are comforting themselves with rising absolute sales while ignoring their shrinking share of the total wallet. IGD’s data confirms that the channel’s slice of total grocery spend is forecast to shrink even as absolute global convenience sales head toward the trillion-dollar mark by 2030. That is not a contradiction—it is an explicit boardroom warning. The channel is growing in size but shrinking in operational relevance because operators are still merchandising like scaled-down supermarkets instead of competing directly like agile QSRs.

“The lived reality on the forecourt floor is immediate. NACS data reveals that foodservice now generates nearly 39 percent of in-store gross profit from just 28.5 percent of sales. Yet, roughly a third of your convenience shoppers are still peeling off to visit a dedicated QSR within thirty minutes of leaving your pumps. That is over $100 billion a year walking straight out of your network into the hands of competitors who simply built a superior food proposition. RaceTrack didn’t waste time debating this execution gap; they bought Potbelly Sandwich Works outright. Every operator without an aggressive foodservice-led format review right now is choosing to keep funding a competitor’s growth.”

Global Frameworks:

Navigating Regional Retail Realities

Convenience does not metamorphose the same way twice. Boardrooms operationalising this immediate-consumption pivot must adapt to four highly distinct regional realities:

Europe (The Mobility Retail Micro-Format):

Delivering the strongest projected share gains in IGD’s global forecast. Forerunners like REWE Group and Żabka Group are scaling tiny-format nodes inside mobility networks—fuel stations, EV charging hubs, and transit interchanges—built from the outset exclusively around single-serve, immediate-consumption missions rather than shrunken grocery ranges.

United States (Foodservice as the Battleground):

US convenience is now explicitly competing with the QSR sector for the exact same trip, not just the same consumer. Foodservice’s share of the industry’s $340-billion-plus in-store sales continues to climb, and the blockbuster RaceTrac–Potbelly acquisition signals the new enterprise playbook: buy restaurant capability outright rather than attempting to build it organically in-house.

Asia (Scale Without Penetration):

Forecast to contribute the largest absolute increase in convenience sales globally, yet modern brand penetration remains below 8 percent. Hyperlocal traditional wet markets and independent retail continue to compete fiercely—a stark reminder that ‘convenience’ as a channel category translates entirely differently once you leave Western retail infrastructure.

GCC (Premium Format, Extreme Climate Convenience): Growth is heavily shaped by an extreme climate driver. Intense heat pushes shoppers toward premium, highly air-conditioned immediate-consumption formats at fuel and mobility hubs even for short journeys, with upscale foodservice concepts weaponised as the primary differentiator against fragmented independent operators.

World-Class Execution: The Immediate-Consumption Paradigms

The Scale Paradigm (Buc-ee’s): Buc-ee’s, Ltd. proves definitively that immediate consumption is not restricted to small-footprint real estate. Their travel centres routinely exceed 50,000 square feet yet operate entirely on a food-for-now operational logic, decoupling the old assumption that store size dictates customer mission. As leading

US retail strategist Brittain Ladd has argued, grocery and convenience operators who treat micro-fulfillment as their only strategic priority are missing the broader disruption: the accelerating consumer shift toward prepared, ready-to-eat food that competes directly with the restaurant trip, a structural reality that the RaceTrac–Potbelly deal validates in real capital terms.

The Micro-Format Paradigm (Żabka): Demonstrating the opposite end of the geometric spectrum. Instead of scaling the physical box, Żabka scales network density, deploying tiny-footprint automated and modular nodes across urban transit layers to place an immediate-consumption point everywhere a consumer has a spare six minutes.

The Executive Priorities: Capitalising on the Mandate

Foodservice as the Primary Category Core: Restructuring category management, kitchen throughput, and supply chain cadence entirely around foodservice as the dominant profit driver, rather than treating it as a secondary aisle bolted onto a shrinking grocery core.

QSR-Grade Format Economics: Evaluating strict build, partner, or acquire pathways into restaurant-grade foodservice capability—following the precedent RaceTrac has set—rather than incrementally upgrading legacy hot-food display cases.

Decoupling Format From Mission: Redesigning physical store footprints—large or small—around the specific consumption occasion of the immediate location, rather than defaulting to a rigid, single national box size.

The Convenience Benchmarks

Foodservice Gross Profit Contribution (38.9%): The percentage of in-store gross profit dollars now generated by foodservice from under a third of total sales—the clearest P&L proof that food, not fuel, is the channel’s real margin engine.

QSR Trip Leakage (~$100BN): The massive annual food-dollar value convenience operators currently lose to quick-service restaurant competitors within minutes of a forecourt visit.

Immediate-Consumption Sales Window (60 Minutes): The definitive Circle K operational benchmark for the proportion of in-store merchandise consumed within an hour of purchase.

Impact Thinking: The 18

Month Reality

“The convenience operators who win the next 18 months will be the ones who stop asking whether they are a grocery format with food on the side, and start operating as a restaurant with a forecourt attached. Foodservice is no longer a category—it is the entire business. Build your kitchen throughput, your format economics, and your supply chain around that single operational fact, and the trillion-dollar convenience opportunity becomes yours to take rather than the QSR sector’s to keep taking from you.”

Week 25–30: The Executive Roadmap

Week 25: The Sentient Store – Vision AI as the Operational “Eye”.

Week 26: Social Commerce & The Point of Purchase Revolution.

Week 27: The Convenience Channel – Micro-Format Growth and Out-of-Home Calories.

Week 28: Fashion’s Data Dividend – First-Party Personalisation at Scale.

Week 29: Pharmacy & Health Retail – The Next Retail Media Frontier.

Week 30: General Merchandise – Rebuilding Basket Value in a Discount-Led Market.